Frequently Asked Questions (FAQs)

There following are frequently asked questions relating to Assessment and Taxation. Please click on any of the following “questions” to bring you the details and responses:

Assessment FAQs:

What is property assessment?

Property assessment is the process of assigning a dollar value to a property for taxation purposes. In Alberta, property is taxed based on the “ad valorem” principle. Ad valorem means “according to value.” This means that the amount of tax paid is based on the value of the property. The municipality is responsible for ensuring that each property owner pays his or her fair share of taxes. Property assessment is the method used by municipalities to distribute the tax burden among property owners in a municipality.

What is the relationship between property assessment value and property taxes?

Too often, the terms “assessment” and “taxation” are considered to be interchangeable. However, assessment and taxation are very different. Although one impacts the other, each is a distinct and independent process. “Assessment” is the process of placing a dollar value on a property for taxation purposes. This value is used to calculate the amount of taxes that will be charged to the owner of the property. “Taxation” is the process of applying a tax rate to a property’s assessed value to determine the taxes payable by the owner of that property.

What is the Alberta model of property assessment and taxation?

The assessment and taxation system begins with government policies that are outlined in the Municipal Government Act. All activities that are associated with property assessment and taxation are governed by this legislation. The assessor interprets these rules to determine which valuation method must be used for each property. An assessor collects a variety of information to calculate a property assessment.

Once the assessment is complete, the assessed value is entered on the assessment roll, which lists all of the property assessments in a municipality. Assessment notices are created from the information on the assessment roll. A notice is mailed to every property owner in a municipality. If property owners do not agree with the assessed value of their property as listed on their assessment notice, they can appeal their assessment. The assessment roll is used to calculate the amount of municipal and education property tax payable on each property.

What is market value?

The market-value-based standard is used to determine the assessed values for the majority of properties in Alberta. Market value is the price a property might reasonably be expected to sell for if sold by a knowledgeable, willing seller to a willing buyer after appropriate time and exposure in an open market.

Key characteristics of market value are that it is the most probable price, not the highest, lowest, or average price. It is expressed in terms of a dollar value. It assumes a transaction between unrelated parties in the open market. It assumes a willing buyer and a willing seller, with no advantage being taken by either party. It recognizes the present use and potential use of the property. Sometimes the market-value-based assessment of a property is confused with the sale price of an individual property. It is important to note that the market-value-based assessment is not the sale price. The sale price is an historical fact. The sale price is the amount the purchaser agrees to pay and the seller agrees to accept under the circumstances surrounding the sale.

What is assessed?

Not all property is assessable for property tax purposes. The Municipal Government Act outlines what property is assessable for taxation. The Act defines property as:

- > A parcel of land

- > An improvement

- > A parcel of land and the improvements to it

- > It does not include things like furniture, jewellery, automobiles, or other personal possessions. If a property cannot be assessed, this means it cannot be taxed.

Properties that are not assessed or taxed include:

- > Publicly owned infrastructure or equivalent

- > Privately owned facilities

- > Minerals Property in Indian reserves

- > Property in Metis settlements

- > Growing crops

Who prepares assessments in Alberta?

Assessments for all types of property are prepared by professional, certified assessors. Assessors receive training in a variety of areas including property valuation techniques, legislation, and quality assurance. Under provincial legislation, a municipality must list at least one designated assessor. A designated assessor is responsible for completing a number of tasks laid out by provincial legislation and regulations. An assessor is hired by a municipality in one of two ways: as an employee of the municipality, or as a contractor. Contracting often occurs in smaller municipalities where the duties associated with calculating assessments are not a fulltime activity. Regardless of the assessor’s employment situation, all assessors, whether they are contractors or municipal employees, must follow the same procedures and legislation.

What are the property owners’ rights to assessment information?

Just as assessors abide by rules when collecting information for assessment purposes, taxpayers have a legislated right to know how their assessment is determined. A municipality is required to provide sufficient information showing how the assessment of a property was prepared. “Sufficient information” means that the municipality must provide enough information to explain to an assessed person how the assessment was prepared. In addition, the assessed person has the right to see the assessment roll, which lists the assessed values for all properties in the municipality. If requested to do so, a municipality must provide an assessed person with a summary of the assessment of any assessed property in the municipality, as long as the municipality is sure that confidentiality will not be breached.

A municipality may charge a fee for providing this information. The assessed person is also entitled to see the assessment record, a listing of property characteristics for his or her own property, and the assessment roll. The ability of an assessed person to see his or her assessment, check the facts, and compare his or her assessment with other property assessments makes the assessment system more accessible, fair, and understandable.

What is the assessment roll?

An assessment roll is a listing of all assessable properties in a municipality and their assessed values. The Municipal Government Act requires each municipality to annually produce an assessment roll. The roll must be completed by February 28 each year. The assessment roll must contain the following information for each assessed property:

- > Assessed person (owner of the property), including name and mailing address

- > Location Property type assessed (land, improvements, or land and improvements)

- > Description of the improvement being assessed (pipeline, structure, etc.)

- > Assessed value

- > Assessment class

- > School support declaration

- > Taxable status (total or partial exemption from taxation)

What is the assessment notice?

Assessment notices are created from the information on the assessment roll. The assessment notice is the document that municipalities send to property owners to tell them about the assessment of their property. An assessment notice must include the following information:

- > All of the same information as appears on the assessment roll

- > The mailing date

- > The date by which a complaint must be filed if a property owner is challenging an assessment

- > The name and address of the designated officer with whom a complaint must be filed

Each year every municipality is required to send an assessment notice to every assessed person listed on the assessment roll. Each municipality must publish a notification in one issue of a local newspaper to announce that the assessment notices have been mailed to property owners within the municipality. Sometimes an error is found on an assessment notice. The assessed person can contact the assessor to correct this information. Corrections can only be made to current-year assessment notices. This means that a person cannot change an error, omission, or wrong description on an assessment notice from a previous year.

Each property in a municipality receives an assessment notice whether it is exempt from assessment and/or property taxation or not. If an assessed party believes that his or her property should receive an exemption from assessment, property taxation, or both, then the property’s exemption status can be challenged through an assessment appeal.

What is the assessment complaint and appeal process?

To ensure that property owners have a voice in the property assessment system, the Municipal Government Act has set out a complaint and appeal process for property owners who have concerns about their assessment. The process involves two levels of formal appeal. The first is at the municipal level with an assessment review board (ARB), and the second is at the provincial level, with the Municipal Government Board (MGB).

The first step an assessed person should take if he or she believes his or her property assessment is unfair or inaccurate is to contact the assessor. The assessor can be reached by calling the municipality’s office at the number listed on the assessment notice. The assessor may be able to inspect the property to determine if an error was made. The assessment can be corrected if necessary. If the assessor agrees that the original notice is not accurate, a new notice can be issued.

If the assessor and the property owner cannot come to an agreement, the property owner can begin the formal complaint process by filing a complaint with the local assessment review board. An assessment complaint must be filed using the Government of Alberta’s “Assessment Review Board Complaint Form” (form number LGS1402), or provided by your municipality upon request. You can also download it from the Municipal Affairs’s website at: www.municipalaffairs.alberta.ca

Once you have filed an assessment complaint with the assessment review board, the municipality is no longer required to fulfill a section 299 or 300 request for information until after the complaint has been heard and decided upon.

Additionally, Municipal Affairs has published and updated a number of guides:

- > Guide for the Exchange of Assessment Information: Market Value Properties

- > Guide to Property Assessment and Taxation in Alberta

- > Filing a Property Assessment Complaint and Preparing for Your Hearing

If you have any further questions about assessment and taxation legislation or processes, please contact the Assessment Services Branch at lgsmail@gov.ab.ca, or by calling Municipal Affairs at 780-422-1377.

What is the Assessment Review Board (ARB)?

The assessment review board is the first level of formal complaint for all types of property assessments except linear property. The assessment review board is a local board. Its members are appointed by the municipality. Each municipality has its own assessment review board. These boards are local because assessment and taxation are municipal responsibilities, not provincial responsibilities. The assessment review board is a quasi-judicial administrative board. This means it is created, empowered, and staffed according to the legislation laid out in the Municipal Government Act. The board is like a court as it can order something to be done. In this case, it can order a change to the assessment on a property.

Who can make a complaint?

Any assessed person, taxpayer, or person acting on behalf of an assessed person or taxpayer may file an assessment complaint. If ownership of a property changes while a complaint is in progress, the new owner of the property or business then becomes the assessed person or taxpayer in relation to that property or business. This person may become involved in any proceeding before the board.

Complainants must demonstrate that the assessment of their property is not a fair estimate of the price the property would sell for on the market. Preparing a case for the complaint hearing will take some time and research. Property owners who are considering filing a complaint should consult Alberta Municipal Affairs’ guide, “Preparing for your Assessment Complaint or Appeal Hearing.” As well, complainants should contact their assessment review board office for details about the process that must be followed and the information that has to be provided.

What a complaint can be about?

A complaint may be filed about any of the following items listed on the assessment or tax notice:

- > Description of the property or business

- > Name or mailing address on the notice

- > Assessment of the property or business

- > Assessment class or subclass assigned to the property (this can affect the tax rate)

- > The type of property

- > The type of improvement

- > The school support listed

- > Whether the property is assessable

- > Whether the business or property is exempt from taxation

The assessment review board cannot hear complaints about the amount of the property tax bill or the municipality’s tax rate. Assessment review boards cannot change the tax rates or the services provided by the municipality. If a property owner has specific concerns about these issues, he or she can discuss them with the municipality’s administration or Council.

How to file a complaint?

Complaints must be filed in writing on or before the deadline shown on the assessment notice. The complaint must include:

- > Written reasons for the complaint

- > The complainant’s mailing address

- > The appropriate filing fee must be delivered or mailed to Vulcan County. These fees are outlined in our current Fees for Service Bylaw, to view these Bylaws, please see our Fees for Service Bylaw section.

If an assessment notice and tax notice are combined, the deadline for filing a complaint is on the tax notice. Municipalities must give the assessed person a minimum of 60 days to file a complaint. Once the complaint has been filed, the assessment review board clerk will schedule a date for the complaint hearing. At the hearing, the complainant will present his or her case to the board. The assessor for the municipality generally attends the hearing to present information on behalf of the municipality. After hearing all presentations, the assessment review board may announce its decision at the hearing if the members believe they can make an immediate decision. If the board does not make a decision at the hearing, the decision will be mailed to the complainant at a later date. All decisions of a municipality’s assessment review board must be made within 150 days of the mailing of the municipality’s assessment notices.

What is the Municipal Government Board?

Sometimes those affected by an assessment review board decision (property owners, assessors, etc.) are not happy with the decision made by the assessment review board. If this is the case, an appeal of the decision may be filed with the Municipal Government Board. The Municipal Government Board is also a quasi-judicial administrative board. Members of this board are appointed by the province, not the municipality.

Appeals to the Municipal Government Board must be filed within 30 days of receiving the written notice of the assessment review board’s decision. At the Municipal Government Board hearing, the complainant is required to make a presentation similar to the one that was made to the assessment review board. The Municipal Government Act provides that the decisions of the provincial board are final in matters relating to property assessments. Points of law may be appealed to the Court of Queen’s Bench and pursued through the Alberta judicial system.

What is the impact of assessment complaint or appeal decisions?

It is important to note that any decision an assessment review board or the Municipal Government Board makes is for the current year’s assessment only. This means that the decision does not apply to previous assessments, nor will it be applicable to the next year’s property assessment. For example, if the assessed value of a property is decreased as a result of a board’s decision, it will not result in adjustments to previous years’ assessments, nor will it have any bearing on assessments that are prepared in the future.

Taxation FAQs

What is a tax rate?

The tax rate is used to calculate your annual tax levy and it reflects the amount of taxes required for every $1 of assessment. The tax rate is also referred to as the mil rate.

The tax rates are set each year by County Council. To view the current tax rates, please see our Tax Bylaws section.

Any interested ratepayer is welcome to sit in on the Council meeting and/or submit their concerns to County Council by way of a letter. The tax rate is usually set in the month of May, however this can change. Please call the Administration office at (403) 485-2241 for confirmation of when the tax rates will be on the Council Agenda.

What are the other outside requisitions?

Outside requisitions come from organizations for which Vulcan County collects tax dollars. The organizations we collect for at this time are:

- > Province of Alberta School Taxes (education requisition)

- > Marquis Foundation (senior housing foundation requisition)

- > Royal Canadian Mounted Police (RCMP requisition)

- > Designated Industrial Property (DIP requisition) – only for DIP type properties

- > Waste Authority

How are the tax rates calculated?

The tax rates are calculated by dividing the total amount of revenue required in the current budget by the total assessment of all taxable property within Vulcan County.

How can I estimate my taxes?

To estimate your property taxes you would multiply the market value (purchase price) of your property by the current tax rate. Please note that market value does not apply to farmland and we would recommend that you call the assessment officer in order to get the current assessed value of your farmland.

Please note that the County also has created a “Property Tax Calculator” to assist in estimating your taxes. Please see our Property Tax Calculator section for additional details.

When are tax notices mailed?

Tax notices are mailed on or before May 31 of each year, with taxes due July 31 of each year. All property taxes in the Province of Alberta are based on the assessed value as of December 31 of the previous calendar year. All property taxes pertain to the current calendar year, so even though notices are mailed May 31, the billing is for property taxes due for full, current calendar year (Jan 1 – Dec 31).

When are property taxes due?

Property taxes are due July 31 of each year. If July 31 is a Saturday or Sunday, then the following Monday would be the deadline. To avoid penalties your payment must be post-marked on or before July 31 (or the deadline date). If you are mailing your payment on July 31, please ensure that the Post Office places a readable date stamp on the envelope. If we cannot read the date, you will be assessed the current penalty.

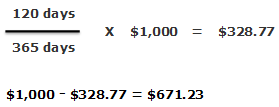

How would I prorate my taxes if I sell my property?

It is not the responsibility of Vulcan County to adjust property taxes when a property is sold, this should be done by the lawyers handling the property sale transaction. To prorate your taxes you would take the number of days of the current year that you have owned your property, divide this number by 365 and multiply by your tax levy.

Example: If your property was sold May 1 and your tax levy was $1,000:

Your share of the property taxes would be $328.77 and the purchaser’s share would be $671.23.

Does Vulcan County have a tax prepayment plan?

Yes, we do. You can obtain forms by calling or visiting our Administration Office or by e-mailing our tax department. Forms are also available online. A ratepayer can be added to the program at any point during the year; however, the account may not have any tax arrears and the deadline for applying for current year taxes is July 1. Payments are removed from your account on the 15th or the 30th of each month. The payments for January – June of each year are based on the prior year’s taxes and the payments from July – December are based on the current year’s taxes. Please see our Tax Installment Payment Plan (TIPPs) section for additional details.

What are the benefits of being on the tax prepayment plan?

The major benefit is that you do not have to pay a potentially large bill in one lump sum. The other benefit is that you have 12 months to pay your taxes and there are no penalties assessed against you. Please see our Tax Installment Payment Plan (TIPPs) section for additional details.

Why do I have to pay Education taxes?

The Provincial Government has mandated that all municipalities will collect school taxes on behalf of the provincial government. Every property owner in the province pays school taxes, regardless of whether they have school age children or not. Questions pertaining to the Education tax should be directed to the following:

- > Alberta School Foundation Fund

- > Palliser Regional Division No. 26

- > Horizon School Division #67

- > Christ the Redeemer School Division No. 3

Can I designate my school taxes to the Separate school division?

Yes, you can, within certain areas of Vulcan County. School taxes can only be designated to a separate school division, if your property lies within that division. In Vulcan County only a small portion of the west boundary of the County lies within Christ the Redeemer School Division No. 3. If you purchase property in this area, a School Support form will be sent to you by our tax department. If you do not live within the division, your taxes are automatically designated to support the public division (Palliser Regional Division #26 or Horizon School Division #67).

When a separate school district exists, individual property owners within that district who are Roman Catholic must direct their property taxes to the Roman Catholic separate school district and individual property owners who are not Roman Catholic must direct their property taxes to the public school district.

I own a property in another jurisdiction, why do I have to pay school taxes again?

Every taxable piece of property in the Province of Alberta is assessed school taxes, regardless of whether the owner owns one (1) piece of property or 100 pieces of property. This has been mandated by the Provincial Government through legislation.

Can I find out what my neighbors’ taxes are?

No, you cannot. This is private information and is not available to anyone else unless authorized by the taxpayer.

Can I find out my neighbors’ assessment?

Yes, you can. The assessment roll is available for viewing at the County Administration Office. These fees are outlined in our current Fees for Service Bylaw, to view these Bylaws, please see our Fees for Service Bylaw section.

The County also utilizes web-based interactive mapping; where it allows for online viewing of the County maps and provides many details relating to the maps (such as a summary of assessment information). To view our web-based mapping, please see our Maps & Addressing section.

If you have any additional questions on assessment or taxation, please feel free to contact our Office at 403-485-2241.